Problems With Social Security: And Why You Should Not Soley Rely On It For Retirement

According to the annual 2019 Social Security and Medicare Board of Trustees Report, social security will be paying out more benefits than it generates revenue in 2020.

The government will have to tap into social security’s reserves to cover benefits and, without reforms to the program, these reserves will be depleted by 2035, the report says. When the reserve runs out, tax revenue will only be able to pay 80% of the benefits.

Rising costs are a sign of the increase in the number of Americans aging into the program, the report continues. Approximately 10,000 baby boomers become eligible to collect social security benefits every single day. As a result, costs will continue to overshadow income and accelerate with each passing year.

This report paints a sobering picture of the program’s financial condition, but this does not mean social security will go away. It does, however, mean that millions of Americans relying on social security will get less if left unaddressed.

Despite the plain-as-day problems with social security, lawmakers are reluctant to make changes. Congress can either pass laws to keep benefits at the same level (increasing the country’s deficit); raise the age of Americans getting benefits; or increase payroll taxes. Someone will lose with these changes, which is why social security reform is often referred to as the third rail of American politics.

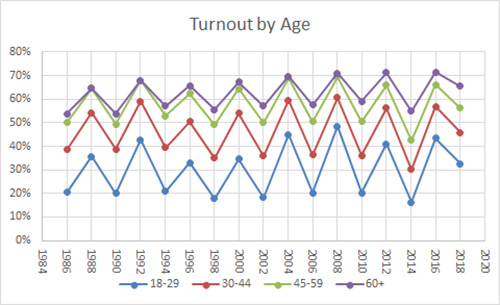

To put ‘third rail politics’ into perspective, there are currently 46 million retired workers (65 years and older) on Social Security. Benefits from social security make up 61% of their income, and a third of these retirees rely on it for 90% or more of their income. Since Americans aged 60 years and older make up the largest voting age group to turn out for elections, it is not hard to understand why our (elected) lawmakers are hesitant to address social security reform. Touch it and risk political suicide.

Social Security Is Not Being Used As Originally Intended

It is clear social security faces serious challenges, which is precisely why Americans should not solely rely on it for their retirement income. However, the average working couple has only saved $5,000 for their retirement. And only one-third of working Americans save money in an employer-sponsored or tax-deferred retirement account, according to the U.S. Census Bureau. Experts believe this is part of the problem. Americans are not saving and depend too heavily on Social Security for their retirement income. Upon its creation in 1935, social security was designed to be a safety net for elderly Americans who had no financial support. It was not intended to be a sole source of retirement income.

How Can A Pre-Retirement Age Worker Avoid Retirement Crisis?

One long-term solution to consider is investing in Whole Life, Universal Life or Indexed Universal Life policies in your pre-retirement years. These policies are considered permanent life policies and can be used to save for retirement. Permanent life policies provide a death benefit as well as accumulate savings. Part of your premium payment goes toward a death benefit to protect loved ones in the event of your untimely death. The other portion builds up cash value on a tax-deferred basis. As you make payments, cash earnings grow and are guaranteed to increase over time. Permanent life insurance policies are not at risk of market volatility, like 401(k) plans are.

The key to these policies is to begin investing as soon as possible to start accruing cash value. When you are ready to retire, you can borrow against portions of the cash value as a tax-free loan. The dividends earned are considered a return of the premiums you have been paying the entire life of the policy. The dividends are only taxable if they exceed the premiums paid.

You can also combine life insurance with a long-term care rider to create a Hybrid Policy. The life insurance protects your loved ones with a death benefit, while the long-term care rider allows you to use all or a portion of the death benefit for qualified long-term care expenses.

Other Financial Options

Life Insurance Questions?

We hope that this information on social security and retirement is useful to you.

If you’d like to learn how we can help you plan your retirement, call Empower Brokerage at (888) 539-1633 to speak to one of our Life and Annuity experts or leave a comment down below.

Get affordable life insurance quotes by clicking here.

See our other websites: